Kathmandu: Shankar Group, one of Nepal’s largest and most prominent business houses, has long stood at the intersection of scale and controversy. While the group’s disputes often grab headlines, its financial structure—particularly its heavy reliance on bank financing—has now come under sharper focus.

Over the past decade, the group has rapidly expanded its business, reaching close to Rs 100 billion annually. In parallel, it has become the largest borrower in Nepal’s banking system, with credit limits exceeding Rs 121 billion and actual borrowing estimated at around Rs 80 billion.

In principle, businesses rely on external financing—either through bank loans or public debt instruments—to expand operations, create jobs, and generate profits. However, questions arise when a group with such massive borrowing does not rank among the country’s top taxpayers. Critics argue that the group’s expansion has been disproportionately driven by debt rather than internal capital strength.

This raises a broader concern: how have banks extended loans nearly matching the scale of the group’s business? Oversight responsibility lies with Nepal Rastra Bank, though its role in monitoring such exposure has come into question. The issue is not merely regulatory—it directly impacts public deposits held within the banking system.

The situation has intensified following the arrest of key figures, including chairman Shankarlal Agrawal and vice-chairman Sulav Agrawal. Investigations are ongoing, with another senior figure, Sahil Agrawal, also under scrutiny. These developments come shortly after the arrest of businessman Deepak Bhatt on allegations of misusing public funds for share trading.

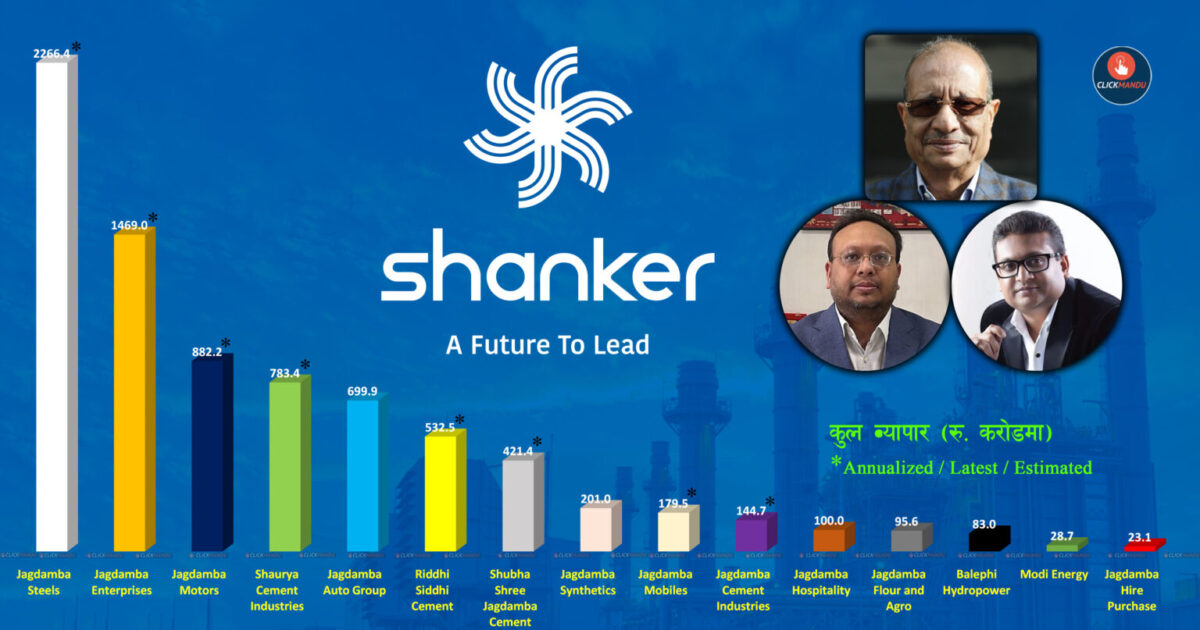

Founded around 90 years ago, the group has diversified investments across insurance, steel, cement, automobiles, FMCG, hydropower, hospitality, and more. It operates roughly 40 companies, with around 15–17 major firms forming the backbone of its financial structure.

Data from rating agencies suggest that 15 companies alone report a combined turnover of about Rs 80 billion. Given the group’s broader network, the actual कारोबार is likely significantly higher. Notably, some companies have reportedly stopped sharing financial data with rating agencies amid declining performance—an indicator of rising financial opacity and potential banking risks.

The group is internally divided into two major operational arms: Jagdamba Holdings, led by Sulav Agrawal, and Jagdamba Group, led by Sahil Agrawal. Together, they oversee a wide portfolio of industries.

Among key companies, Jagdamba Steels—once Nepal’s largest steel producer—has seen a sharp decline in revenue, dropping from Rs 49.7 billion in 2022 to Rs 29.7 billion in 2024. Similarly, Jagdamba Mobiles’ कारोबार has steadily decreased over recent years, while Jagdamba Motors has also shown fluctuating performance.

On the other hand, some segments, such as Jagdamba Auto Group and Jagdamba Hire Purchase, have demonstrated growth, reflecting uneven performance across the group’s portfolio. Cement companies like Shaurya Cement and Riddhi Siddhi Cement continue to generate multi-billion-rupee revenues, supported by partnerships with other major business houses.

The group’s exposure to debt is spread across 18 banks and financial institutions. According to central bank sources, over a dozen companies linked to the group have been approved for loans exceeding Rs 100 billion, with actual utilization nearing Rs 80 billion.

Loan sizes range from Rs 800 million to Rs 8 billion per institution. Major exposures include Jagdamba Steels (Rs 33.15 billion), Shaurya Cement (Rs 14.87 billion), Riddhi Siddhi Cement (Rs 11.94 billion), Jagdamba Enterprises (Rs 15.81 billion), and multiple hydropower and hospitality ventures.

Overall, the group accounts for roughly 1.5 percent of Nepal’s total banking sector lending, which stands at around Rs 5.8 trillion. While this may appear proportionally small, the concentration of exposure across interconnected entities raises systemic risk concerns.

As investigations into the group’s leadership unfold, regulators have reportedly tightened monitoring of its loan portfolio. The central question now is not just about the group’s financial health, but whether Nepal’s banking system has adequately managed its risk exposure to one of the country’s most powerful conglomerates.

Comment Here