Kathmandu: Until a few years ago, the cheque was the undisputed and most powerful medium of payment in Nepal’s financial market. From real estate transactions to large-scale commercial deals and government payments, checks dominated the landscape.

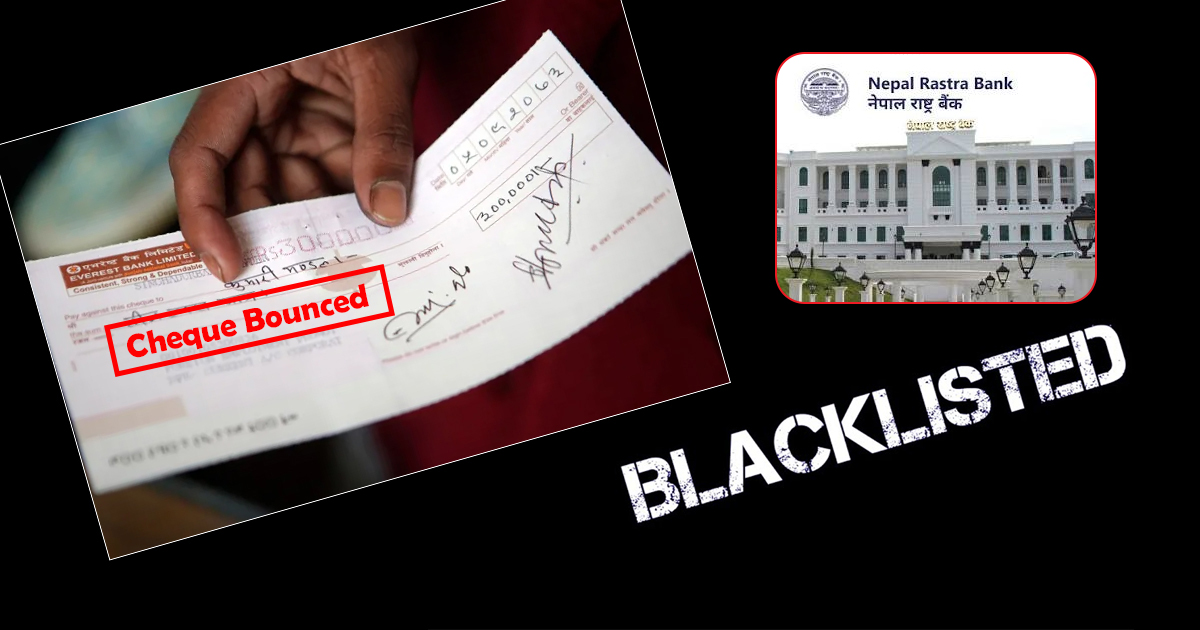

However, as technology has advanced, the check is increasingly becoming more of a liability than a solution. Following a surge in the misuse of checks and an alarming rise in the number of citizens being blacklisted, Nepal Rastra Bank (NRB) has begun policy preparations to either completely phase out or drastically overhaul the existing cheque system.

The current situation regarding the financial blacklist is dire. According to recent data, the number of individuals blacklisted by the Credit Information Bureau for violating financial discipline has reached approximately 170,600. This figure represents about 0.6 percent of Nepal’s total population. Being blacklisted carries severe consequences; these citizens are not only barred from taking bank loans but are also frequently deprived of various government services and facilities.

Data from the Bureau confirms that while around 27,700 are microfinance defaulters, the remaining 142,900 are mostly those who defaulted on bank loans or, more significantly, issued checks without sufficient funds in their accounts. Reports indicate that between 65 and 70 percent of all blacklisted individuals are listed specifically due to check bounces.

For the fiscal year 2081/82, out of nearly 130,000 newly blacklisted individuals, a staggering 74.8 percent were categorized under check bounce. These statistics confirm that in Nepal, the check has transformed from a payment instrument into a weapon that pushes citizens into criminal records and financial exclusion.

While a check is intended solely as a medium of payment, it is frequently misused as a form of collateral or guarantee.

Recognizing that this misuse is the primary driver behind the rising blacklist numbers, the central bank is reconsidering the necessity of bearer and account payee checks. While “Good for Payment” checks may remain, NRB officials believe that using checks as guarantees has fostered a toxic culture. Many individuals issue post-dated checks with the mindset that if the payment isn’t settled, they can simply use the police and the legal system as a debt collection agency, leading the central bank to explore alternative guarantee systems.

Under current Nepalese law, a check bounce is considered a banking offence. Legal proceedings typically begin if a check is bounced three consecutive times due to insufficient funds. According to the Banking Offence and Punishment Act, those found guilty must pay the check amount plus interest, and can face up to three months in prison, fines, or both. Furthermore, the offender is blacklisted, which effectively freezes their future financial transactions and prospects.

Recent supervision reports from the central bank further highlight that checks now pose a significant financial risk. The reports describe checks more as a “source of risk” than a “means of payment.” Systemic vulnerabilities include banks still using manual stamps for “Good for Payment” checks instead of system-generated prints, which increases the risk of forgery. There are also reported delays in clearing processes and security lapses where sensitive items like chequebooks and ATM cards are kept under single-lock systems instead of the required dual-control protocols.

Supervision has also uncovered instances where loan funds are immediately transferred to the accounts of directors or related parties via checks without proper monitoring of the loan’s intended purpose. Furthermore, banks have been criticized for submitting incomplete or incorrect customer data to supervision systems, making it difficult to track credit limits and prevent check misuse. With over 150,000 people now entangled in issues related to non-payment or insufficient funds, the administrative burden on banks to record and verify these disputes has become immense.

The central bank and legal experts have noted that the check has essentially become a modern version of a predatory informal loan deed, known locally as “Kapali Tamasuk.” People often exchange blank or post-dated checks to build “trust” in transactions where funds do not yet exist. This reliance on checks for informal lending has not only increased administrative hurdles for the banking sector but has also created a crisis of confidence in the entire financial system.

To combat this, the central bank is considering a revolutionary “Force Loan” mechanism. Under this proposed system, if a check is presented and the account lacks funds, the bank would pay the recipient and then book that payment as a “forced loan” against the account holder. The bank would then take responsibility for recovering the funds from the account holder through instalments or collateral liquidation. This ensures the payee receives their money immediately while preventing the payer from being instantly criminalized and blacklisted.

Additionally, the central bank plans to issue strict guidelines that determine check issuance based on a customer’s credit history, income levels, and transaction limits. For example, salary account holders might have their check limits tied to their monthly income. The push toward this reform is also supported by the rapid expansion of digital payments in Nepal. With QR code transactions now exceeding 129 billion rupees per month, the relevance of physical checks is fading.

While phasing out checks overnight is challenging due to gaps in digital literacy and internet access in rural areas, the global trend is clear. Countries like Singapore have already discontinued corporate checks, and their use is negligible in Europe and the US. Reflecting this shift, the Nepal Rastra Bank’s monetary policy for the upcoming years aims to introduce specific provisions to reduce the barriers created by blacklisting, ensuring that check bounce does not permanently strip citizens of their access to essential banking services.

Comment Here