Kathmandu: In recent years, Nepal has seen a surge in new investment plans as people seek better returns on their money. With interest rates remaining low, traditional bank savings offer minimal gains. At the same time, the stock market is often viewed as too risky or time-consuming for many, especially those with limited financial literacy.

As a result, individuals are increasingly exploring alternative investment options that promise higher returns. However, compared to global markets where diverse financial instruments are widely available, Nepal’s investment landscape has long been considered limited, with many options either high-risk or accessible only to those with substantial capital.

That trend, however, is gradually changing. Modern investment tools that have gained popularity internationally are now entering the Nepali market, expanding opportunities even for small-scale investors.

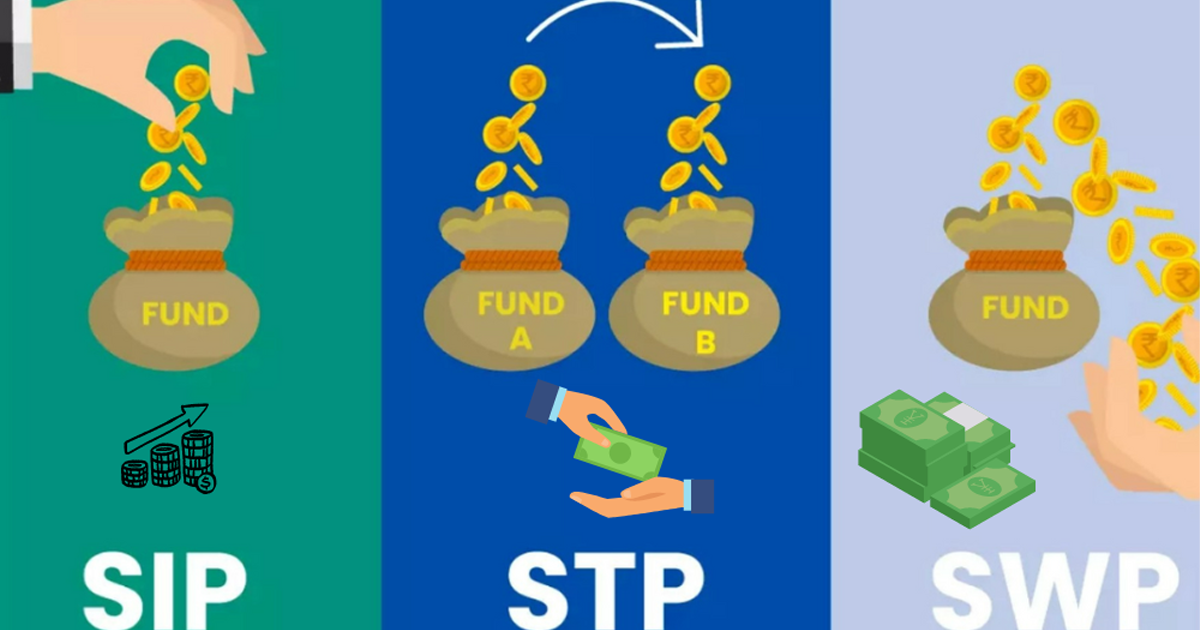

These innovations are not only diversifying investment choices but also reshaping how people save and manage their finances. Among these, the Systematic Investment Plan (SIP) has already established itself as a widely accepted tool over the past eight years. With the expansion of open-ended mutual funds, most asset management companies now offer SIP schemes, and their number has steadily grown.

A SIP allows investors to contribute a fixed amount at regular intervals—monthly, quarterly, or semi-annually—into mutual funds. This disciplined approach helps investors navigate market fluctuations by averaging costs over time, buying more units when prices are low and fewer when prices are high.

It promotes financial discipline and supports long-term wealth creation through the power of compounding. Particularly suitable for salaried individuals, SIPs enable gradual accumulation of wealth even from small, regular savings, making them one of the most accessible investment tools in Nepal today.

As SIP gains popularity, attention is also shifting toward complementary strategies like the Systematic Withdrawal Plan (SWP). Unlike SIP, which focuses on regular investment, SWP allows investors to withdraw a fixed amount periodically from their accumulated funds. This makes it especially useful for generating a steady income stream, similar to a pension. For example, instead of keeping a lump sum idle in a bank account, an investor can place it in a mutual fund and withdraw a fixed monthly amount while the remaining balance continues to grow. SWP can be used either with a lump-sum investment or after building a fund through long-term SIP contributions.

The appeal of SWP lies in its ability to provide regular cash flow while still benefiting from investment returns. It is particularly valuable for retirees or individuals seeking a consistent income without exhausting their capital too quickly. Even as withdrawals are made, the remaining investment continues to earn returns, allowing the fund to sustain itself over a longer period if managed wisely. However, effective use of SWP requires careful planning, discipline, and a clear withdrawal strategy.

Another emerging concept in Nepal’s investment space is the Systematic Transfer Plan (STP), which is gradually gaining attention as a smart financial strategy. STP involves transferring funds from one mutual fund scheme to another at regular intervals. Typically, investors first place a lump sum into a relatively safe debt fund and then systematically transfer portions into higher-return equity funds over time. This approach helps reduce the risks associated with market volatility and avoids the pitfalls of investing a large amount at once during unfavourable market conditions.

STP is particularly useful for managing large sums received from bonuses, asset sales, or remittances. By gradually shifting funds into equity markets, investors can benefit from cost averaging while maintaining a balanced risk profile. The process is automated, reducing the need for constant manual intervention, and offers flexibility through different variations such as fixed, flexible, and capital appreciation transfer plans.

Overall, these three tools represent a new wave of financial thinking in Nepal. SIP encourages disciplined saving and long-term investment, SWP enables efficient and sustainable withdrawal of accumulated wealth, and STP helps strategically deploy large sums while managing risk. Together, they provide a more structured and intelligent approach to personal finance, marking a significant shift in how Nepalis are beginning to build, use, and grow their money.

Comment Here